Most Recent Posts

Amazon’s Fight With IRS – At Least It Gives People Work

Perhaps the simplest thing would be to tax public companies based on their reported earnings. The foreign tax credit prevents double taxation. By taxing the companies on their reported earning instead of having one set of accountants scheming how to inflate earnings to help stock prices and another set of accountants over in the tax department scheming on how to reduce taxable income, the pressure would be to tell a consistent story. The IRS could to a significant extent ride on the work of the independent auditors and tax provisions would be comprehensible to more than a few hundred people in the country. On the other hand, a plan like that would probably be a job killer for accountants, so maybe it is good to keep things as they are. At least it gives people clean jobs with no heavy lifting.

Finally Something About The Baby Holm Controversy

I met Bob Baty thanks to my coverage of the fight over the dubious constitutionality of Code Section 107 the parsonage exclusion. He became my most constant commenter...

Mixing Penny Stock With New Cryptocurrency Does Really Not Improve Either

Ernie Land and I have spoken and been in correspondence for several years. Mostly it has been about the trials and tribulations of young earth creationist Kent Hovind, who served a long term in federal prison and who was spared an additional long term by sharp legal work for which Ernie gets a lot of credit. I believe that Ernie is about as sincere as a person with a sales related career can be. On the other hand, Ernie seems to sincerely believe many things that I find preposterous. And visa versa. Kent Hovind’s innocence narrative , evolutionary biology, the age of the earth and a variety of conspiracy theories are among the things that Ernie and I agree to disagree on while maintaining a cordial relationship. Sunshine Capital and Dibcoin will now join that list.

Florida Man Goes From Multilevel Marketing To Cryptocurrency – What Could Possibly Go Wrong?

More than anything else Dibcoin reminds me of a short story by Poul Anderson titled Fairy Gold which is nicely summarized here. A young man is rewarded for helping an elf with fairy gold. Fairy gold is just like real gold at night but turns into trash when the sun rises. A series of transactions occur. The last one is by the hero’s former girlfriend who sells her grandmother’s business before the coin goes poof, but it is fine because now she can live happily ever after with the hero. I’m sure a feminist critique of the story would find it problematic, but that’s not going to bother Poul Anderson who died in 2001.

There’s Still Time To Fund A Roth IRA For Your Underemployed Millennial

Rosen Associates has over 700 dental practices in its client base. The Roth IRA for kids is part of their standard repertoire with the added wrinkle of, when appropriate, finding things that youngsters can do around the office. The idea works not just for twenty-somethings but even for tweens. I found this story by Natali Morris who pays her three year old and five year old for doing things like putting stamps on mailers and shredding. That might be getting a little carried away. Also I would explore potential impact on financial aid, before doing this for kids not yet through college.

The Devil And Lois Lerner

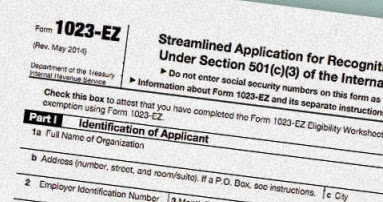

When people asked me about applying for exempt status for fairly modest organizations I generally advised that I thought that the game might not be worth the candle. Looking at how simple Form 1023-EZ has made things, I’m rethinking that. For a long time, I have believed that the dose of credibility that organizations get from having 501(c)(3) status was largely unfounded. The new process means that it should confer no credibility at all. If someone implies that their 501(c)(3) status is somehow a seal of approval, you need to put your bs detector on high alert. A storm is coming.

Quadratic Equations And Tax Benefits David Rockefeller In Tax History

I often remark that you learn all the math you need to do tax work by the fourth grade. Here was a possible exception. Tax preparers with New York clients would have to dust off their high school math. I actually had a client who got hit with the New York minimum tax, so this was not just a Rockefeller level problem. (David Rockefeller had federal AGI of $7.7 million in 1976. In 1976, if I had eight dollars in my wallet, I thought I was ready for anything.

Math challenged tax preparers were spared relearning the quadratic formula by the Commission’s ruling that noted there was no authority in the statute for using New York AGI rather than federal AGI in computing the preference and no “tax benefit” rule. Another illustration of Reilly’s First Law of Tax Planning – “It is what it is. Deal with it.”

Blog Cited In Appellate Brief In Form 1099 Case

Forbes magazine also published an article about the District Court Opinion, noting with some concern that it made the decision about whether or not to issue a 1099 much more complicated. Peter J. Reilly, Pulling IRS Into Your Business Dispute Might Not Be Such a Good Idea, Forbes (July 25, 2014)

Stop Telling Me To Drink On St. Patrick’s Day

My St. Patrick's Day crusade which started out positively is turning nasty. The original idea was that people of Irish descent on the day that the common cultural has...

No, President Trump Didn’t Escape Income Taxes For 18 Years

Of course it is mostly explained by the alternative minimum tax (AMT) which shows up on Line 45. Even though the AMT is reflected as an add-on to the regular tax, it is actually a parallel system with fewer deductions and credits, slower depreciation and a lower rate. A reasonable inference from the $36,571,795 on Line 46 is that Trump’s Alternative Minimum Taxable income was in the $130 million neighborhood. He would have had a different net operating loss for AMT purposes than for regular tax purposes and there might be substantial depreciation difference. Form 6251 would explain it.