Most Recent Posts

New York Times Analysis Of Trump’s Tax Position Misses A Lot

What is most disconcerting to me about this particular Times piece is that it does not really appear that Trump was getting away with that much. He did not get a principal reduction from the bondholders, so requiring him to pick up ordinary income at that point would have really been kicking him when he was down. And he did give up equity in return for the more favorable debt terms. Unlike the Son of Boss shelters that would be coming later, everything about this was real. There were real casinos that lost a ton of money. After the restructuring there was as much principal as there had been beforehand and some equity had been surrendered.

Jill Stein Finds It Is Not Easy Being Green

My speculation for the cause of her reticence was that details in her returns that were fairly mundane would, seen through glasses with Green lenses, appear quite shocking. Dr. Stein’s mother, Gladys Stein, died in 2010. Assuming conventional estate planning, assets accumulated not only during her parent’s lives, but also. possibly, something from her grandfather who invested in Chicago real estate might leave some traces on her 2012 or 2013 returns.

It probably does not hurt Mike Pence that he had an ownership interest in a chain of gas station convenience stores, but if Jill Stein owned something like that even on a transitory basis, there would be somebody at the Green Party convention calling for her to make reparation. That was my thinking, anyway. We’ll probably never know.

Law Professor Calls Trump’s Tax Losses Fake

There is something else to consider. Apparently, that 1995 Trump return was one of the last ones prepared by Mitnick. Given Trump’s involvement in public companies, there is a pretty good chance that his return has like Romney’s been done by one of the major national firms since then.

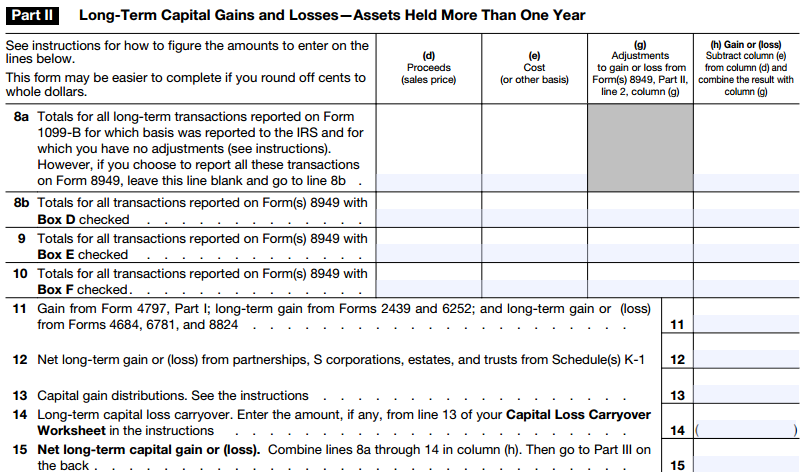

And here is the thing about net operating losses. Trump did not deduct the loss in 1995, he got to carry it forward and commentators assume that he must have used it in subsequent years. The net operating loss is a deduction in the year that it is used. Even if the statute is closed on the year of the loss, the IRS gets a bite at it in the year that it is used. More importantly, for this discussion, the preparer of the return can’t just rely on the prior accountant having it right.

Trump Had A Point About His Own Taxes In The Debate

The only two roles I could see for Trump in public accounting are client from hell or managing partner. Public accounting firms at the regional and large local level tend to be run by somewhat sociopathic dictators of greater or lesser benevolence. Hillary Clinton on the other hand could be the leader of a peer review team or one of the people in a national firm that has a job not involving direct client service coming up with nonproductive things for working people to do. Clinton is definitely the Big Four type. Trump not so much.

How Much Do Public Companies Pay In Income Taxes?

In computing its reported earnings under Generally Accepted Accounting Principles BH provided for a deduction from reported earning (pretax $34.9 billion) of $10.5 billion in income taxes – 30%. This is explained in some detail in Note 15 (Income Taxes), where you will find that the largest element in the difference in the provision from the hypothetical 35% is the special treatment of dividends received by corporations.

In Note 13 (Supplemental cash flow information) you will find that the amount actually paid for income taxes was $4.5 billion- 12.9%. The relationship between the provision and the amount paid is similar in the previous two years.

The Tax Deduction That Donald Trump Loves And Warren Buffett Probably Likes

The loophole Hillary Clinton is referring to came out of the Supreme Court Gitlitz decision. I’m skeptical that Trump took advantage of Gitlitz. The loophole would have benefited Mike Pence, whose “at-risk” carryover from the cigarettes and gasoline went up in smoke. Pence also voted for the act that closed the loophole, probably costing himself around $100,000. whether he knew it or not

Donald Trump’s Deep Love Of Tax Depreciation – An Affair To Remember

The managing partner is at least moderately sociopathic and a dictator of greater or lesser benevolence. He, and it is almost always a “he”, is charged with the responsibility of making sure his partners don’t give away the store to clients and staff. At any rate, the deal is that they get what the managing partner thinks they deserve with enough grease thrown in to stop them from squeaking too much.

It goes without saying that Trump is the managing partner in the enterprise, although he would probably prefer something more reflective of his value, maybe God-Emperor. On the asset side, there is no such thing as accumulated depreciation. That is because an asset under Donald Trump’s umbrella can only go up in value.

Trump And Clinton Returns And What Regular Folk Need To Know About Carryovers

When Donald Trump’s return was handed off by Jack Mitnick in 1996 or 1997, there was probably very good documentation of his regular tax NOL which we know was in the $900 million range. I would not bet that there was great documentation of the AMT NOL. I may be selling Mitnick short there, but the guy had software that could not handle a nine-digit number, so it is very unlikely that, at that point, it was tracking the AMT NOL for him. That was still relatively early in the computerization of individual returns and there were lots of problems with carryovers.

The Unintended Tax Loophole That Might Have Saved Donald Trump Big Bucks

What strikes me as improbable is that there was an S Corporation that held enough of the Trump empire to facilitate a nearly billion-dollar free basis step-up that does not show up in the public record anywhere. Like the proverbial economist who stranded on an island suggests that he and his companions “assume a can opener”, Lee Sheppard assumes an S corporation. While it might be common to use an S corporation as a 1% general partner, that would not be enough to pull this off. At least in my experience, you don’t want to have the bulk of a real estate investment in an S corporation, because, unlike a partnership, you don’t have basis in the entity’s indebtedness making me less inclined to assume an S corporation, particularly since no one seems to be putting forth a candidate.

Donald Trump’s 1995 Return And A Lesson In Unrealized Appreciation

Buried in all these maneuvers is an aspect of our tax system that while being the feature that probably most contributes to wealth inequality is seldom remarked on. Unrealized appreciation is never subject to income tax. And when I look at the top people in the Forbes 400. I see lots of unrealized appreciation starting with Bill Gates with Microsoft and Warren Buffett with Berkshire-Hathaway (which I should note makes up a very large percentage of my unspectacular net worth)

Real estate turbocharges the unrealized appreciation feature since you are allowed depreciation deductions on real estate and real estate is one of the easier things to leverage. But for it all to not fall apart your real estate better appreciate if you are heavily leveraging it.