Most Recent Posts

Wealth Tax – Constitutional Probably – Good Idea Not So Much

Whatever else a wealth tax accomplished, it would be a significant transfer from the upper-upper class to the upper-middle class. I would think that in some of the larger law and accounting firms, there are already people pitching planning techniques to beat the entirely hypothetical tax.

And if it does pass, the resulting regulations will be of mind-numbing complexity. Just for starters. What do you do about trusts? Do trusts pay the tax themselves with beneficiaries allowed to apportion their unused exemption to the trust? Or is the trust wealth somehow apportioned among the beneficiaries? However it is done, let the games begin.

And then there is valuation. Don’t get me started. And if it is a net wealth tax, what counts as a liability? Think that is easy. Read about partnership taxation.

Dressage Trainer Complains Of Tax Court Mansplaining

Judge Holmes did a holistic analysis of the horse activity and also did the factor by factor analysis that is called goofy by some. He notes that Ms. McMillan had a horse called Goldrush who was retired from competition but still had breeding potential. She had not bred him for quite some time but hoped that things would be better if she sent him to Australia. Unfortunately, he died in 2008. Judge Holmes did not note that Ms. McMillan had Goldrush’s semen frozen, so there was still an afterlife of breeding potential in 2010.

Tax Court Approves Penalty But Does Not Allow IRS To Pile On

Photocredit Pixabay - Pexels Originally published on Forbes.com. Just because somebody believes things that I find preposterous and even harmful, doesn't stop me from...

IRS Drubbed In Tax Court On Partnership Interest Deductions

As it turned out, William Lipnick never received any of those debt-financed distributions. The distributions had gone to his father Maurice Lipnick, who had transferred some of the interests to Willam during his lifetime with the balance passing after his death in 2013.

This made William’s relationship to the partnership debt different than his fathers. To William, the debt was part of his acquisition basis in the partnership. For Maurice the debt traced to however he happened to spend the money – likely making it investment interest. For William, the debt traces to his acquisition of the partnership interest making it deductible against the partnership income allocations.

The Beast I Found In The Park

There are things that annoy me a lot. People mixing up principal and principle or e.g. and i.e. American flags touching the ground or continued being flown after they...

Rubber Hitting The Road On New Partnership Audit Regime

The Games People Will Pay

Most of the reasons I can think of for not electing out of CPAR involve shenanigans that are even worse than the one I imagine that I and my imaginary friend James would play on the Millenials. Assume you don’t elect out and do some really aggressive stuff in 2018. Keep the partnership alive, barely, but by the time it gets around to the adjustment year, the only partners are a couple of moribund C corporations.

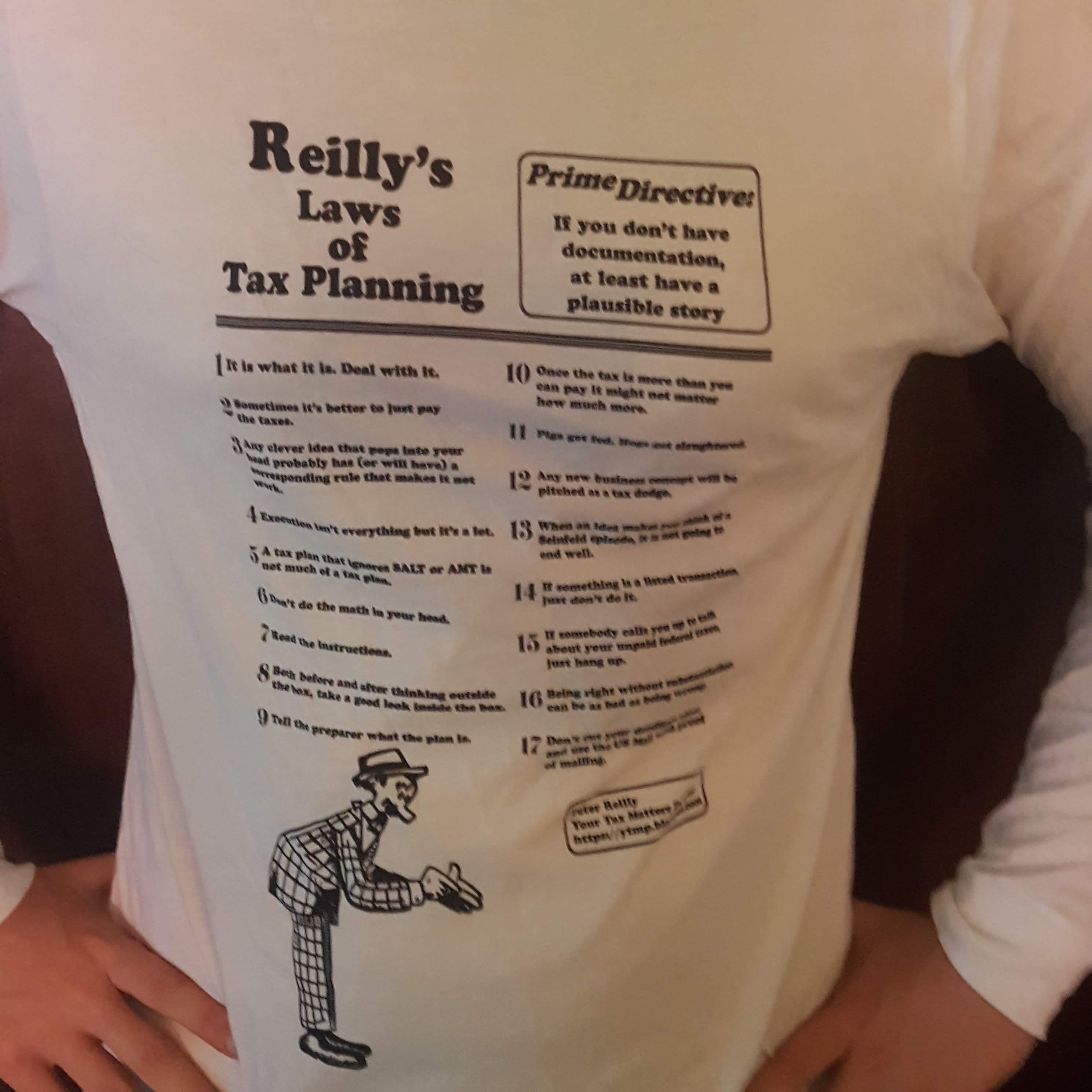

Remember Reilly’s Third Law of Tax Planning – Any clever idea that pops into your head probably has (or will have) a corresponding rule that will make it not work. So maybe shenanigans like that will be foiled. I hope so.

Who Is That Masked Man? DC Circuit Tells Tax Court To Keep It Quiet

I think what would be money well spent by the IRS is to go into the Big 4 and large regionals and hire away the people with ten years or so of experience who know they are never going to be partners because they lack soft skills and will make lousy salespeople. You give them a better work-life balance, a pension and the chance to show up all the corners that they know are being cut. It will strike terror in the hearts of corporate tax departments.

A really radical proposal would be to require public companies to disclose their tax returns as part of their SEC submissions and require the independent auditors to cover them in their opinion. That is more of an entertaining thought experiment than a realistic proposal

What Happens When You Are A Full Year Resident Of More Than One State

And if someone can afford to take on the trappings of two different domicile identities – sophisticated New Yorker and Connecticut Yankee or whatever – maybe it is fair that they pay full tax to each state. Manhattan has a lot of infrastructure to support, you want to make out you are a New Yorker, pay up.

Hobby Loss Roundup And A New Law Of Tax Planning Announced

It is rooted in one of the earliest and most significant 183 decisions, the first time 183 was discussed by an appellate court. It concerned Maurice Dreicer, a trustafarian who spent years (and hundreds of thousands of dollars) searching for the perfect steak. The Second Circuit ruled that the Tax Court had used the wrong standard in denying Dreicer’s losses.

We hold that a taxpayer engages in an activity for profit, within the meaning of Section 183 and the implementing regulations, when profit is actually and honestly his objective though the prospect of achieving it may seem dim. Because the Tax Court applied a different standard, we reverse and remand for redetermination of Dreicer’s deduction claims.

Even on that standard, Dreicer still lost, but that is neither here nor there.

IRS Should Not Be Worrying About Do Not Call Registry

The Tax Court opinion of Judge Daniel Guy in the case of Giving Hearts, Inc. illustrates a waste of IRS resources and focus that is the result of our choice to have the wrong agency regulate not-for-profit organizations. If bad acting by an exempt organization is facilitating significant federal tax avoidance, having the IRS on the case makes a lot of sense. Other abuses of not for profit status should be dealt with by the agency whose business it is to deal with that particular abuse. That’s my takeaway. Here is the story.