Most Recent Posts

Ninth Circuit Pulls Back Big IRS Victory Issued After Judge’s Death

But, but, but, the case is not a win for the IRS as of today. It is back in limbo. Because unlike the stories you hear about Chicago, it seems that in the Ninth Circuit they don’t want the dead to vote. One of the two votes in favor of the IRS was cast by Judge Stephen Reinhardt who died on March 29, 2018, almost four months before the decision issued.

Pay Your Taxes!

So this will be a longish introduction to a really long piece. I will start with the disclaimer that the views expressed by Johnny Cirucci (below the dotted line) are...

Lesbians Want A Church Of Their Own And IRS Approves

Originally published on Forbes.com. Pussy Church of Modern Witchcraft might strike you as something you would find in the Onion, rather than here on a Forbes tax blog,...

Janet Yellen and the Economic Impact of Gender Discrimination

By all accounts, Janet Yellen was more than qualified for the position is Chair of the Federal Reserve. Her PhD in economics is from Yale University. From 1994 to 1997 she was on the Federal Reserve Board of Governors. In 1997 she served as Chair of Bill Clinton’s Council of Economic Advisors. From 2004 to 2010 she was the President and Chief Executive Officer of the Federal Reserve Bank of San Francisco (there are twelve regional reserve banks and San Francisco is the second-largest by assets held, next to New York). She worked her way up in the Federal Reserve after an impressive career and education at the top U.S. schools in economics. Yet, she was confirmed in the Senate by the narrowest margin in history.

The Federal Reserve is tasked with two goals: maximize employment and stabilize prices (inflation). The biggest argument against Janet Yellen for her confirmation was she was a “dove”. A “dove” refers to someone whose economic policy favors low unemployment above the inflation goals. The opposite of a “dove” is a “hawk” whose focus is more on inflation than unemployment. Yellen’s goal was unemployment and during her tenure, there was one of the largest drops in unemployment during any Federal Chair’s tenure. And the other mandate, of keeping inflation stable, she did.

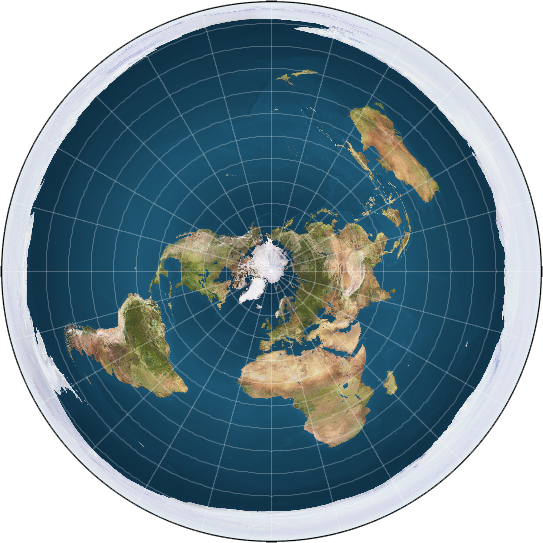

Hovindologist Down The Flat Earth Rabbit Hole

Lamar Smith is back from an assignment. I asked him to look into the odd interaction of Kent Hovind and flat earth. The way this connects with tax is kind of...

We May Have To Wait A Year For Decision In Michael Jackson Estate Tax Case

The intensity of the coverage of the Tax Court proceedings in the Jackson case may be unprecedented. There are occasions when Tax Court decisions break out of the tax ghetto into the mainstream. A notable example was Anietra Hamper, a TV anchor who tried to deduct her undergarments. But the Jackson case. Wow. Richard Rubin has written an article about the writing style of Judge Mark Holmes who is handling the case.

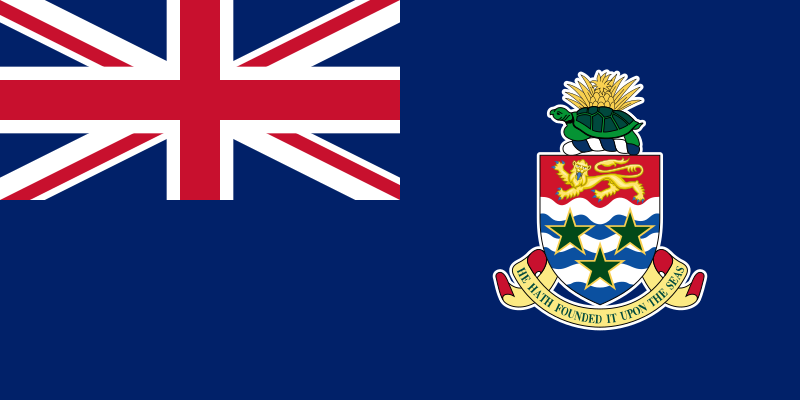

Ninth Circuit Decision For IRS Affects Shifting Of Income To Tax Havens

In order for the IRS to respect the allocation of income between the Cayman subsidiary and the parent, the cost-sharing arrangement to keep and improve the intangible assets needs to pass regulatory muster. One of the requirements of the regulations is that stock-based compensation be included as one of the costs. The taxpayers argued, well enough to convince the Tax Court and one of the three judges on the panel, that in an arms-length deal parties would never include stock-based compensation. The IRS did not deny that, but argued that the regulations could never replicate comparable transactions among unrelated parties because they don’t happen enough.

You generally don’t have somebody thinking they want to find somebody in a small country to buy the right to their intellectual property which they will then license back for use in the rest of the world. Further there will be a cost revenue split on future developments. You pretty much only do that sort of thing with related parties to save taxes or possibly for asset protection or some other regulatory concern. In an arms-length deal you could not consider stock-based compensation since there is a chance that the other party’s stock could really take off.

Law Professors Argue That Housing Tax Break For Ministers Is Unconstitutional

The housing allowance statute results in substantial entanglement between the government and churches, such as requiring the IRS and courts to determine which beliefs or purported beliefs should count as a religion for tax purposes, what constitutes a church or a minister, and ministerial functions, whether an ordained minister working for a secular nonprofit counts as a minister if she gives one sermon a year, and similar quandaries. The tax professors point out that ministers working not in churches but as teachers, counselors, directors of business services, alumni relations, and even as basketball coaches, now qualify for the exemption. “In sum, Section 107 requires the government to investigate and oversee both churches and ministers, delving into both doctrine and practice,” the brief states.

Marijuana Industry Faces Challenging Tax Regime

Traffickers are not taxed on their gross receipts because of 280E. They are entitled to a deduction for what they pay for their product – cost of goods sold – because we have an income tax, not a gross receipts tax. The deduction for ordinary and necessary business expenses (Code Section 162)- like gas for your vehicles, bribes to the police, bullets and rent on safe houses- is a matter of “legislative grace” and can be denied because, you know, drugs are bad like they teach you in the DARE program, that my kids had in elementary school.

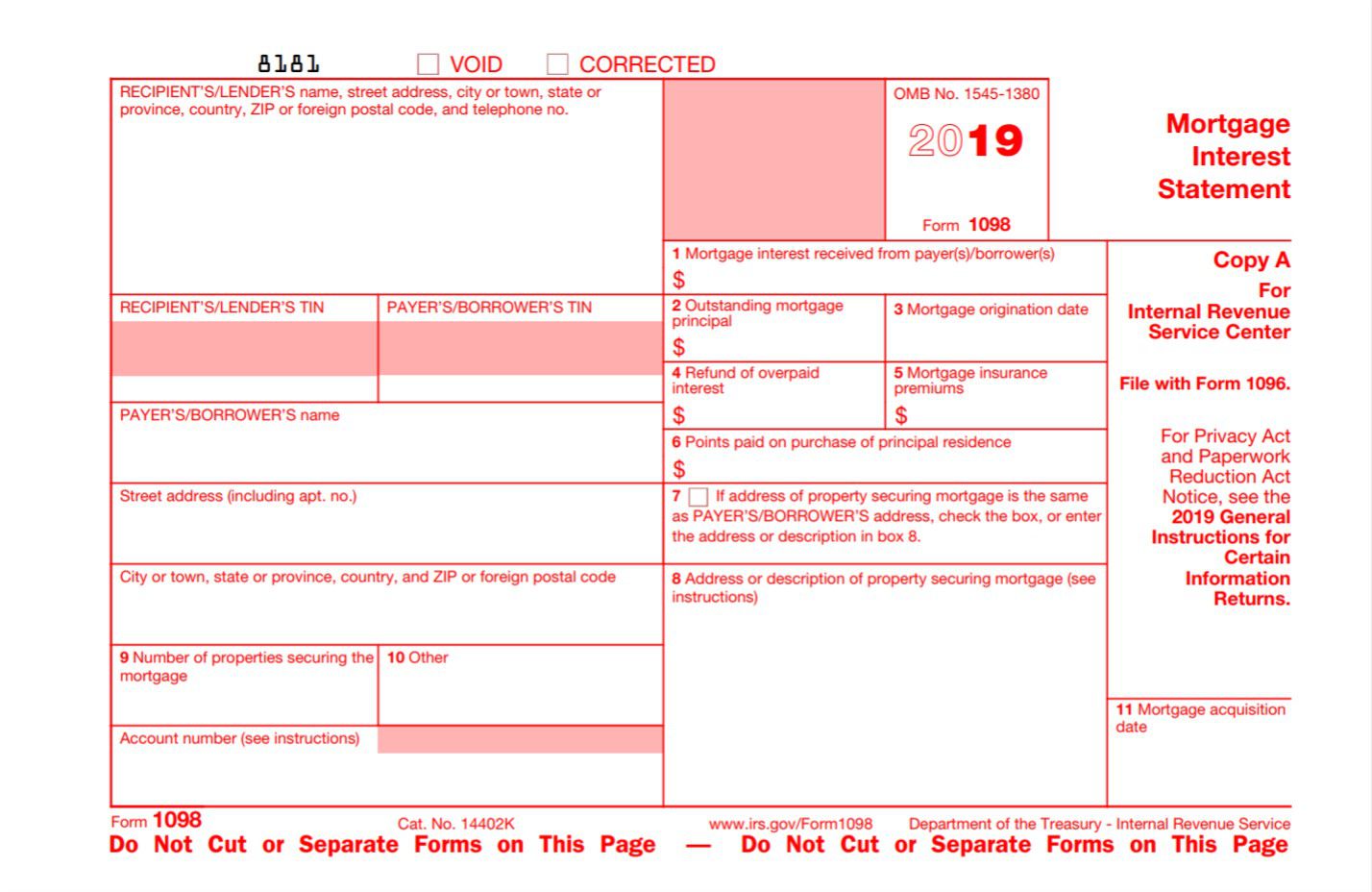

Banks Not Providing Taxpayers With Accurate Mortgage Interest Information

It seems that this problem should really be solved by the IRS. Tell the banks exactly what they are supposed to put on Form 1098 and provide some sort of expedited refund process. It crosses my mind that maybe some sort of catch-up deduction considered as an accounting method change might do the trick including giving relief for closed years.